|

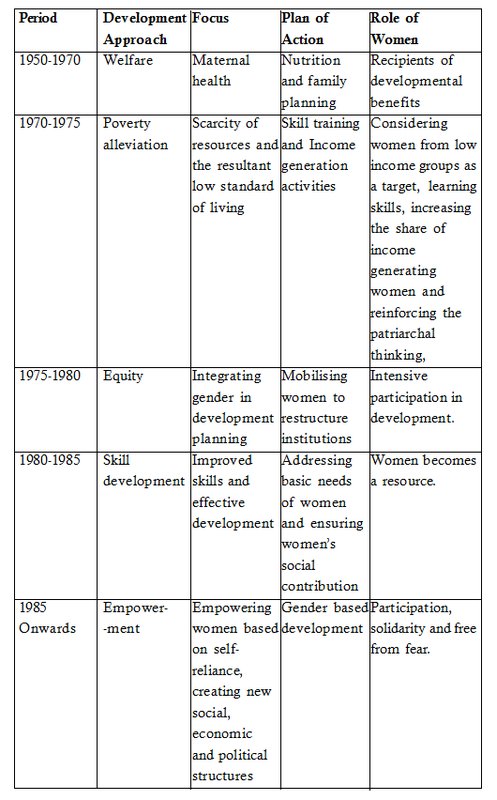

Abstract This article is about the evolution of SHGs in the country and the resultant benefits for the under-served population, especially for women. The SHGs have acquired the status of a movement in India, within a span of three decades, thanks to the sustained efforts of the NGOs, NABARD and the State Governments. SHGs from the simple savings and credit groups have evolved as village levelcommunity based organizations not only to take care of the financial needs of the marginalised communities but also to access various community infrastructures and amenities. This was possible by a process oriented approach. Yet, in recent times, most of the SHGs are targeted by the professional micro finance institutions/agencies (MFIs) for credit delivery, banking on its good repayment history. This massive invasion of MFIs has undermined the habit of regular savings, internal rotation of funds and book keeping, which were the mainstay of SHGs. This is a worrying trend, as SHGs become a target, ignoring the fact that it was a product of process. Self help groups (SHGs) have become synonymous with the grass roots and women development in India. There is no development intervention without involving SHGs. Most of the welfare schemes for the income poor and the marginalised women are dovetailed and routed through the panchayat level federations (PLF) of SHGs. Kudumbashree in Kerala, Sreesakthi in Karnataka, Puduvazhvu in Tamilnadu and Velugu in undivided Andhra Pradesh are a few popular SHG led poverty alleviation intervention by the State Governments.Following the success of SHG movement in the Southern States of India, almost all other States have started replicating the SHG model of intervention, of course with due modifications to suit to the local needs. Genesis of SHGs Self help groups in short known as SHGs are considered as the primary instrument of poverty reduction for the past twenty five years by several agencies (NGOs, International development organizations, donor agencies and Governments). The seed for the concept of SHGs was sown by Mysore Resettlement and Development Agency (MYRADA), a South Indian NGO in the 1980s, by promoting credit management groups (CMGs) wherein they have propagated theimportance of weekly savings among target women and the usage of collected money to issue loans to needy members. MYRADA staff provided training on how to organize meetings, set an agenda, keep minutes, and other areas vital to successful business ventures. The members were often homogeneous in terms of income or of occupation. In 1987, during the implementation of an action research project supported by National Bank for Agriculture and Rural Development (NABARD), MYRADA has re-named them as self help groups. These groups were among the first of their kind, i.e., the self help groups (SHGs) as we know them today. During the same year, PRADAN (Professional Assistance for Development Action) as part of the Rajasthan Government’s poverty alleviation programme, introduced savings in groups which was promoted to provide grant for fodder. Many mahila mandals were formed during the period in States like Maharashtra under the Integrated Child Development Services (ICDS) programme to facilitate the financial access for the poor. NGOs were part of this process to promote mahila mandals and to build their capacities to handle finance. The pilot project of the Tamilnadu Women Development Corporation (TNWDC) in 1989 in Dharmapuri district, with the funding and technical support of International Fund for Agricultural Development (IFAD) was a milestone (State government used SHG strategy for poverty alleviation) in the evolution of SHGs as an institution for women. IFAD invested in training and mentoring of SHGs, building their institutional capacity, which was a new dimension in project design. The institutional support extended by NABARD to SHG promotion and bank linkages as a pilot initiative in 1991-92 has actually given fillip to SHGs.In addition, the successful experiment of TNWDC was not only helpful to massive scaling up of SHGs in the entire State but also emboldened many other States to follow the model for poverty alleviation. Today, the Southern States are standing as models for other States in terms of promotion and nurturing of SHGs and thereby using them for poverty reduction. As per the notification in the website of the Union Bank of India (www.unionbankofindia.co.in/RABD_OTHER_SelfHelpGroups.aspx), Self help group is a homogeneous group of micro entrepreneurs with affinity among themselves, voluntarily formed to save whatever amount they can conveniently save out of their earnings and mutually agree to contribute to a common fund of the group from which small loans are given to the members for meeting their productive and emergent credit needs at such rate of interest, period of loan and other terms as the group may decide. The District Rural Development Agency (drdachamba.org/schemes/SHGs/main.htm) states that SHG is a small voluntary association of poor people, preferably from the same socio-economic background. They come together for the purpose of solving their common problems through self help and mutual help. The SHG promotes small savings among its members. The savings are kept with a bank. This common fund is in the name of the SHG. Usually, the number of members in one SHG does not exceed twenty. While the commercial banks consider SHG membership for micro entrepreneurs, the Government’s thinking is bringing together of poor people, to solve common problems. The commercial banks definition stems from the experience of the Bangladesh model, wherein the micro entrepreneurs are coming together as a group to access financial services. The government’s perspective goes beyond the economic sphere to include overall development. Another practical difference is the way in which SHGs are organised. Both the two definitions talk about the voluntary formation of groups. However, in practice, seldom it happens. In most of the times, the SHGs are promoted by either non-government organizations (NGOs), commercial banks and by various departments of the Governments. NGOs engaged by NABARD to promote and nurture the SHGs are known as self help promoting institutions (SHPI).The scheme still continues to involve NGOs in promotion of SHGs in backward districts.(www.nabard.org/english/SchemePromotion.aspx). The role of promoters varies according to their perspectives of SHGs, and it reflects in the way they conceive the training and development of SHGs. While the banks supported by NABARD focus on skill development and bank linkages for livelihood loans, the State Governments’ women development corporations focus more or institutional development( like panchayat and block level federations of SHG) to take care of common issues. The non-government organizations go one step further and mould them to access their entitlements. SHG: Critical View To understand the way in which the SHGs are currently functioning, we can classify them into two broad categories: First, the SHGs promoted by NGOs and second the SHGs promoted by Government departments. The NGOs promoted SHGs in majority cases ‘’depend’’ on staff members of the NGOs for book keeping, monitoring and linkages with banks and government departments in the name of perfection. Thus they are not functioning as ‘’self help groups’’, rather they are ’’staff helped groups’’. In such cases, if the staff members’ role is diminished or withdrawn, the group slowly dies, for the members are not allowed to operate independently even after a series of training meant for group and fund management. This type of unbroken handholding hinders the growth of SHGs and stumps the opportunities for members to gain self-confidence by doing. The continuous need of the staff handholding creates a client-master relationship between SHG and promoting NGO, and thus closes the opportunity for empowerment. On the contrary, in the Government promoted SHGs, the basic functions are carried out by a few trained members, who also wear various hats (book writer in the group, representative to the panchayat level federation, representative to the block level federation). This sort of consolidation of power in a few hands leads to autocracy in the group and diminishing participation by members who become either ‘’yes’’ members or leave the group. The groups promoted by Government departments have been influenced by the subsidies of loans and the benefits of various social schemes. The continuous pumping of benefits leads to the higher expectations among the members and kills the spirit of self help. Thus over a period of time, the well-intended SHGs become ‘’seek help groups’’ and gradually lose the credibility. Thus they miss the vehicle of empowerment. Empowerment The Oxford Advanced Learner’s Dictionary defines empowerment as giving authority or power to do something. It also states that it is the making of someone stronger and more confident especially in controlling their life and claiming their rights. Empowerment in general refers to encouragement and development of capacities provided to individuals or groups so that they become self-reliant. In social development perspectives, it is the process of obtaining basic opportunities for marginalised people, either directly by those people, or through the help of non-marginalised others who share their own access to these opportunities. It also includes actively thwarting attempts to deny those opportunities. Empowerment is primarily two-fold: sociological and economic. Sociological empowerment relates to the inclusion of marginalised in the decision making process, who usually depend on charity and welfare means to meet their ends, and as such they lose self confidence. In contrast, the economic empowerment relates to the creation of livelihood opportunities for the marginalised and to become self-sufficient. This includes access to funds, market and development of marketable and managerial skills. ‘’The term ‘empowerment’ is now widely used in development agency policy and programme documents, in general, but also specifically in relation to women. ……Central to the concept of women’s empowerment is an understanding of power itself. Women’s empowerment does not imply women taking over control previously held by men, but rather the need to transform the nature of power relations. Power may be understood as ‘power within,’ or self confidence, ‘power with’, or the capacity to organise with others towards a common purpose, and the ‘power to’ effect change and take decisions, rather than ‘power over’ others……… Empowerment is essentially a bottom-up process rather than something that can be formulated as a top-down strategy. This means that development agencies cannot claim to ‘empower women’, nor can empowerment be defined in terms of specific activities or end results. This is because it involves a process whereby women, individually and collectively, freely analyse, develop and voice their needs and interests, without them being pre-defined, or imposed from above. Planners working towards an empowerment approach must therefore develop ways of enabling women themselves to critically assess their own situation and shape a transformation in society. The ultimate goal of women’s empowerment is for women themselves to be the active agents of change in transforming gender relations.Whilst empowerment cannot be ‘done to’ women, appropriate external support can be important to foster and support the process of empowerment. A facilitative rather than directive role is needed.’’ (Reeves and Baden, 2000). SHGs and Women Empowerment The development planning in India, since 1950 has applied many approaches, moving away from the traditional welfare approach to the much talked empowerment approach.The treatment and role of women are varying in each approach, but the appreciable thing is that it is evolving for better.  SHGs could not be viewed as mere savings and credit servicing organizations, for the very idea of SHGs stems from the institutional purview. It is on the firm belief that the poverty is sustained and aggravated not only by the lack of opportunities for the downtrodden and marginalised population, but also by the lack of appropriate institutions and institutional capacities of income poor, the concept of SHGs was coined by the practitioners. Otherwise, practitioners would have simply copied the Bangladesh model of micro credit (mistakenly a large number of NGOs believe that the Bangladesh model is the mother of our SHGs), which focuses only on individual members, though they propagate the five-member small group for micro credit intervention. We accept that the Bangladesh model is useful to address individual household poverty by bringing together the skilled people from low- income groups into a five member group for credit access. The Indian model of SHGs is not only addressing the household poverty, but also addressing community poverty (dearth of community assets/common property resources) when they are properly groomed and guided.

The very word empowerment infers that the entire process is related to the comprehension and application of power, of course, to accomplish the set goals.The opportunities for SHG members to get empowered come when they assume and discharge responsibilities to accomplish their set goals. Therefore the first step is to set achievable goals, orient and capacitate them to assume and discharge responsibilities to accomplish the goals. Since most of the women members of SHGs are either illiterate or semi literate, they need a fairly long handholding (minimum three years, on an agreed withdrawal plan, which describes various role transfers as graduation process) by a well trained team of facilitators. The role of facilitators is critical as they are not supposed to deliver but to enable the members to deliver. The power which is enshrined in the empowerment process is not lying outside the members from low income communities. Rather it is within the member as a potential, but it is clouded and clogged by ignorance, lack of exposure and stimulation. The potential power needs to be unleashed by the promoters of SHGs by conscious and systematic facilitation efforts. The facilitation efforts need to start from the moulding of the staff team. First they need to understand the principles of self help: ‘’It is not that somebody is helping, meaning an outsider is helping, but help comes from themselves’’. It may include mutual help among members and groups. The people from low income groups and marginalised sections expect help or charity in dire situation as they are in a state of powerlessness or helplessness due to chronic poverty. Neither they have confidence in themselves nor have respect for themselves.They are often under a depressive stateof mind, without any hope for future and more worried about today. This is the crux of the issue. Hence, orientation for them should start from creating situations to infuseself respect. Mere providing help in the name of empathy is not going to improve their self worth. It actually destroys their self worth. A person who lost his self worth cannot visualise self respect and the resultant self confidence. It is a tricky situation. The facilitator need to understand this peculiar situation and help them get over poverty but that should be in an empowerment mode. Providing charity is just opposite to empowerment. We can empower a person by sharing information and knowledge, by building their skills and capacities, which would eventually increase their worth and confidence. The facilitator should understand and internalise this fundamental principle while promoting self help groups. In the guise of helping the poor, we should not make them permanent recipients of charity and thereby reduce them as beggars. The SHGs and the women’s empowerment are highly process oriented. Here, I wish to highlight the processes adopted by Centre for Development Alternatives (CFDA), Chennai, a development organization founded in 1990 to promote self help initiatives among women from the underserved population living in the urban fringes of Chennai. CFDA strongly believes that It should start with the identification of the power of ‘’Self’’ and progress towards offering ‘’Help’’ to the needy by functioning as a group. CFDA’s SHG groups are called as ‘’micro bank groups’’ (MBGs). The groups are functioning in 14 villages fall under Citlappakam panchayat union, Kanchipuram district. The MBGs function in a three tier structure: MBGs, zonal clusters (five to ten groups in a particular geographical location) and a federation as the apex body. The federation is known as ‘’Akshaya’’. Under this model, MBGs have complete autonomy to deal with their funds (monthly savings), while the zonal clusters take care of the monitoring of the groups. The federation deals with the good governance and management of MBGs and providing larger loans to MBGs. Under the CFDA model, whenever there is a demand for the formation of a group, the facilitators from the federation ask the interested members to visit the functioning group in the neighbourhood and observe the process. During the observation, they can raise questions and seek clarifications about the purpose and functioning of the group. Thus it serves as a demonstration of a group functioning.Then if they are interested, the facilitator fix a date in consultation with the interested persons for an orientation meeting, wherein the basic rules are once again explained and their concurrence for the SHG formation is sought. On their concurrence, another date is fixed to initiate the group wherein the group is given a name and the roles and responsibilities of members and the functionalities of the representatives (secretary and treasurer) are explained. Then the members are asked to list out the skills requirements of the representatives and accordingly the most suited members are selected to discharge the key roles. Then each member is assigned a role number. There is no president in the group. Instead, there is a chair person on rotation for each meeting. This is to minimise the domination of one person. From the second year onwards, the representatives are selected on rotational basis based on their numbers. There is a performance appraisal system to measure the progress of the groups and its representatives. The performance of the group is linked to the loan limits from the federation, and the performance of the members is linked with the loan eligibility. The performance of the representative is linked with the graduation to the federation, and the performance of the federation representative is linked with the graduation to bank account signatories. Thus a performance oriented system is practised in the groups, which is one of the strong point for the sustainability of the intervention, as a community led and managed institution since 1998. The entire process and indicators of performance were developed and fine tuned with several rounds of inputs from the community. The ideas are floated in the cluster meetings, for further deliberation in the groups and the conclusions of deliberations are consolidated at the federation and again ratified by the groups for implementation. The same process is followed to create, modify and nullify rules of the groups and federation. Though the process is lengthy and takes at least one month to take a decision, it is meticulously followed to empower the community in decision making. Thus a participatory decision making system is established and followed. 1. Enabling Environment for Empowerment The self help promoting institutions (SHPIs) should create an enabling environment to empower women through SHGs. It includes awareness creation about the importance of mobilisation of women, self help, mutual help and encouragement to them to act as a group. There should be opportunities to realise their self worth, air their views, participate in the decision making and creating their own rules and regulations. It is by determining their own governance and management structure, they start taste the empowerment. To create such an enabling environment, the facilitators should respect the members, firmly believe that the members do have resources (knowledge, survival instinct, experience, basic livelihood idea, small amounts of money) and they could be mobilised and groomed for better accomplishments. If the facilitators and promoters of SHGs think that the income poor and socially marginalised cannot understand and comprehend situations and act according to the situations, then they are miserably failed in guiding the needy. The facilitator should start with a positive bent of mind. Then everything is possible. This is what CFDA’s experience. The facilitator may need three to six sittings with the prospective members to mobilise and convert them as SHGs. The second is that we should understand that we are working for a change; from the powerlessness to being powerful, from poor standard of living to better standard of living. Everything is about change. The empowerment process itself is working for change; from the current state to a desired state of affairs. The fundamental principle of change is, it starts with ‘’self’’, like a ripple in the water emanating from the stone thrown. Hence, the facilitator has to change first, from the ‘’provider mind set’’ to a ‘’facilitator mind set’’. The role of facilitator is akin to a midwife helping the delivery of a pregnant woman. She can understand the pains and difficulties of the pregnant woman by experience and persuade the pregnant woman to undergo the process by narrating others’ experience, providing massage, counselling etc. She never attempts to deliver the baby on behalf of the pregnant lady. Nor can she do that. Similar is the role of the facilitator. They should not attempt to deliver results on behalf of the community or the needy members of SHGs, but only help them undergo the due process. This is very essential step in the empowerment process. Then only, the SHG members can own the organization, the tasks and so on. The third is to create opportunities for graduation in the SHGs. Majority of women enter SHG as members and retire as just members. Only a handful are trained and given multiple roles: as members, and representatives in SHG with cheque signatory powers, representatives of panchayat level federation, and representatives of block level federation. ‘’One member-many hats’’ situation. This leads to centralisation of power and disinterest of members, eventually the disintegration of SHG. This is the current situation in most of the SHGs across the country irrespective of the promoters, be it NGOs or State sponsored agencies. This is contrary to the principles of empowerment, where in the ownership, responsibilities and decision making are expected to be shared among all the members. This is happening because the promoters and facilitators are in a hurry to show the results in terms of targets. They need to understand the incubation period required for a SHG to become an organization. Time makes a difference. We allow 21 days of incubation, then the egg hatches and if we allow only an hour, then the possibility is only omelette. This is the logic of incubation. An SHG requires minimum three years’ handholding to become viable and to sustain. Unfortunately the SHG’s maturity is assessed by the end of six months and based on certain rating link it for bank loans. In reality, most of the SHGs’ survival is decided by the members by the end of the first year taking into account the benefits: number of loans, size of the loans, interest earned by the rotation of money in the group, the key person’s attitude and behaviour, etc. 2. Key Role of Capacity Building Capacity building, especially with opportunities for hands on experience (loan processing, loan approval, loan collection, conducting meeting, visiting banks, handling money, taking part in cluster/ federation meetings), makes a lot of difference, especially for the illiterate and semi literate members. Capacity building is also similar to weight lifting. It should start with simple and small tasks. To identify what is simple for one, the facilitator’s observation is important. He/she should observe members during the informal conversation, in group meeting to identify their potential and accordingly groom them. He/she should not expect perfection from the members when they assign a task. Perfection is a dead wood. The facilitator should allow members to make mistakes and use the opportunity to train them better. It should be a learning process, not a condemning process. A learning process is essential for empowerment. With these kind of opportunities, members slowly gain experiential knowledge and use them. 3. Knowledge is Power In the age of information and knowledge explosion, members from marginalised communities and economically deprived need tailor made information regarding the ensuing opportunities relating to livelihoods, health care, sanitation and standard of living. Such opportunities are made available in the meetings of SHGs, class room training programmes, exposure and exchange visits. The inter and intra group learning opportunities are provided to them by show casing both success and failure stories and open it for discussions. By this live process the members are provided with opportunities to ‘’know’’ and ‘’record’’ it in their minds. Then it becomes ‘’Knowledge’’ and used as power. 4. Solidarity is Power Members, by coming together as a group, get opportunities to mingle with others in their own group and the neighbourhood. By frequent interactions they first develop communicative skills and thereafter other interpersonal skills like listening, problem solving and decision making. They quickly learn the power of putting their view points, justifying their needs, convincing capacity in the group meetings while transacting financial business. Gradually they open up to share their family and community matters and look for suggestions to address them. During the process, they understand the limitations of addressing an issue as a person, and try to build solidarity with likeminded persons. Then they start applying the solidarity pressure to resolve issues. Usually it starts with the mode of collecting the overdue from a defaulter. On tasting the success, they try to apply the same logic to help the needy to solve personal and family disputes and thereafter to represent the community needs as a group and start putting pressure on the panchayat to get relief. Thus they realise the power of solidarity. 5. Managerial Power In finance, they learn the regularisation (meetings and funds), documentation (minutes and accounts), systems (loan processing, scrutiny and approval), collective decision making, sequencing of events(attendance, agenda, discussion, decision, documenting, ratification, closing of meetings), transparency (all financial transactions are conducted in the meeting itself) and bringing solidarity pressure to deal with default/delayed payments. They learn and build their capacities by handling financial transactions in the group. Once they identified the success formula they apply it in social sphere to meet their demands. That is how many SHGs were able to get basic amenities (drinking water, link roads, street roads, grave yard, street lights, and improvements in balwadi) for their village. With the evolution of panchayat and block level federation of SHGs, they were able to access various government Schemes/ benefits like pensions, employment under National Rural Employment Guarantee Act (NREGA) and group housing in many villages. 6. Political Power Having tasted the solidarity of the fellow members, ambitious members have developed courage to contest in local body elections and a section of them have been successful. With the associated power of local governance as ward members, their social status has been enhanced in their family and in the community. It has also helped them to get basic facilities for the village. 7. Social Power Traditionally men were powerful in the families in the rural areas by the virtue of their economic dominance. Now, women are gaining a respectful place in the family by mobilising loans through SHGs not only to take care of the consumption needs of the family, but also invest in livelihoods like agriculture, petty trade and small businesses. In many cases, they invest loan funds for the higher education of their children, particularly the girls (many has become engineering graduates) and house construction. These sort of continuous financial support has earned the appreciation and support of their menfolk. Conclusion The penetration of SHGs across the country is an indicator of its relevance and usefulness in bringing women from income poor category and the marginalised sections, to address poverty. ‘’The journey so far traversed by the self help group – bank linkage programme (SHG-BLP) crossed many milestones – from linking a pilot of 500 SHGs of rural poor two decades ago to cross 8 million groups a year ago. Similarly from a total savings corpus of a few thousands of Indian Rupees in the early years to a whopping `27,000 crore today, from a few crore of bank credit to a credit outstanding of `40,000 crore and disbursements touching `20,000 crore during 2012-13. The geographical spread of the movement has also been quite impressive - from an essentially Andhra Pradesh – Karnataka phenomenon in the beginning now spreading to even the most remote corners of India. Over 95 million poor rural households are now part of this world’s largest micro Credit initiative’’. (Suran, 2013). The SHGs, over a period of time has transitioned from addressing household poverty, by providing financial service to the needy members to take on the community poverty and social development issues in the village. This evolution is an indication of empowerment. Women in SHGs first use the mutual help process to address household poverty while they muster the support of other like minded SHGs in the village, by using the platform of panchayat level federation to represent community issues to the local government and get solutions. The interest shown by a few State Governments (like Tamilnadu) to promote SHGs for men reinforces the relevance of SHGs in mobilising the needy to address poverty. The renewed focus on reviving the defunct SHGs under the National Rural Livelihood Mission (NRLM) is another indicator of the relevance of SHG as a grass root institution. NABARD plans to promote 20 lakhs SHGs during 2013-17 to reach the unreached population in 127 resource poor districts in the country adds to the list (Suran, 2013). However, the fast pace development of groups leaves little room for members to internalise the true perspectives (self-confidence-self-respect-self-reliance) and process of empowerment by hands on learning experience. The leader centric training and capacity building is also a stumbling block for the real empowerment. The training should cover all the members. Training the facilitators is also required to equip them to mould the SHGs as self-reliant. References

R. Jayachandran Chief Executive, CFDA, Chennai |

Categories

All

Social Work Learning Academy

50,000 HR PROFESSIONALS ARE CONNECTED THROUGH OUR NIRATHANKA HR GROUPS.

YOU CAN ALSO JOIN AND PARTICIPATE IN OUR GROUP DISCUSSIONS.

MHR LEARNING ACADEMYGet it on Google Play store

|

RSS Feed

RSS Feed

SITE MAP

SiteTRAININGJOB |

HR SERVICESOTHER SERVICESnIRATHANKA CITIZENS CONNECT |

NIRATHANKAPOSHOUR OTHER WEBSITESSubscribe |

MHR LEARNING ACADEMY

50,000 HR AND SOCIAL WORK PROFESSIONALS ARE CONNECTED THROUGH OUR NIRATHANKA HR GROUPS.

YOU CAN ALSO JOIN AND PARTICIPATE IN OUR GROUP DISCUSSIONS.

YOU CAN ALSO JOIN AND PARTICIPATE IN OUR GROUP DISCUSSIONS.

|

|